In-Depth Look: Why Warner Bros. Discovery, Inc. - $WBD Is a Strong Investment

In-Depth Look: Why Warner Bros. Discovery, Inc. - $WBD Is a Strong Investment

This post gives a brief synopsis on why Warner Bros. Discovery is a current holding in Brandon's Portfolio.

Overview/Business Model:

The combination of Warner Media and Discovery created a media titan that can offer a streaming platform that can directly compete with AMZN 0.00%↑ Prime, NFLX 0.00%↑, PARA 0.00%↑and Disney+ with arguably better content. WBD 0.00%↑has been caught up in the terrible sentiment surrounding the streaming industry underpinned by NFLX 0.00%↑ loss of subscribers in the last quarter. During the same quarter HBO Max & Discovery+ added > 3M subscribers. In the recent ER for NFLX 0.00%↑,they announced a subscriber loss of 970,000 during the second quarter, a smaller loss than the 2 million it had projected last quarter. Even though the results were bad the stock rallied suggesting all bad news had been priced in before the earnings announcement. I see this as an indication the worst is behind us for the broader streaming sector.

Quality Content Offering:

Discovery+ content compliments the popular content on HBO max. Combining the 2 into one product will provide a broad content offering for customers and add a lot of value to the company. The combination of Warner Media and Discovery assets creates one of the largest content libraries with ~200k hours of video content. The assets are also quite complimentary, as Discovery is strong in non-fiction content and Warner Media in fiction.

WBD 0.00%↑ has a diverse revenue stream and a majority of their revenue still comes from Linear TV so they are better positioned to weather this inflationary environment than NFLX 0.00%↑. Over the last year there has been a cascade of negative catalysts dragging down WBD 0.00%↑price. But none of these negative catalysts have anything to do with the fundamentals of WBD 0.00%↑. Moreover, management is focused on eliminating unprofitable projects to dial in on content that will lead to margin expansion, signs of an improving business, not a deteriorating one.

Advantages over other Streamers:

Being a cinema first streamer WBD 0.00%↑ gets the added benefit of massive Box Office sales. The movies are highly profitable and provide more value to subscribers who can now stream cinema-quality movies or pay to watch them in theatres. This is not the case for Netflix.

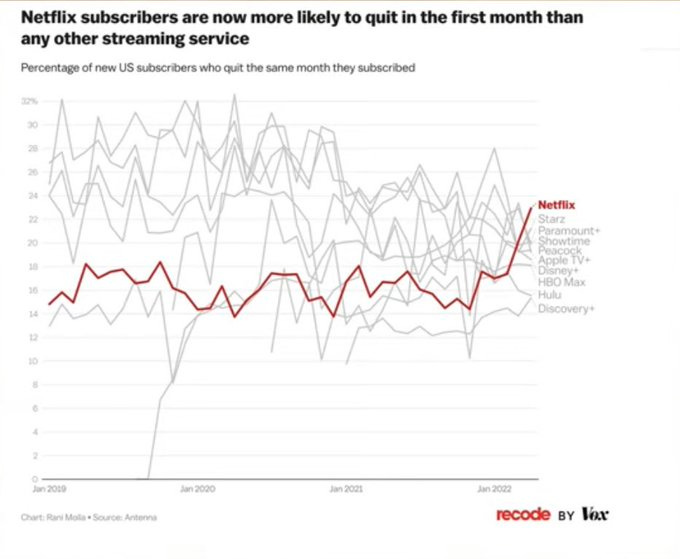

This chart below by Recode shows that Netflix has a much higher churn rate than its peers indicating Netflix customers are not satisfied with the service they are offering and are not willing to pay their elevated prices the entire year just to receive sub-par content.

Insider Activity:

An added benefit to my investment thesis there has been a lot of insider buying in the recent months which indicates management also believes the stock is undervalued relative to fundamentals.

Long-Term Leverage Targets:

The combined company is new so we may need to see a few more quarters of results to know if they are delivering on their planned cost synergies, and DTC growth targets. Strong, well-capitalized competition is one risk to this investment. Consumers have a lot of options to choose from in terms of streamers. It is important that WBD 0.00%↑ differentiates themselves from the competition and provide a better all-around experience. Another risk to the investment is the company's debt level. Total debt is estimated at about $58 billion. With about 5x gross leverage and 2x debt-to-equity fast deleveraging a priority which will take some time. The company also needs to balance investments in content.

Financials/Valuation

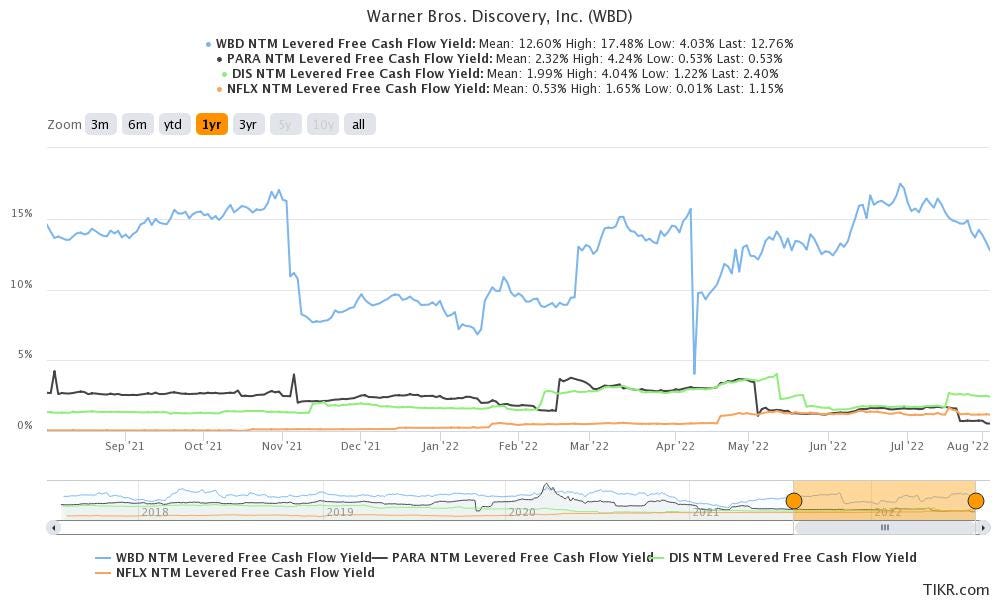

On the announcement of the merger, the combined company projected $14B of EBITDA w/ a 60% FCF conversion. This gives $8.4B of FCF. with 2.43B shares outstanding that equates to $3.46 FCF / share. At today’s price of ~ $14.5 that is a multiple of ~ 4.2x which in my opinion is ridiculously cheap. For context NFLX 0.00%↑, DIS 0.00%↑, PARA 0.00%↑ & WBD 0.00%↑ NTM FCF Yield are 1.22%, 2.62%, 0.74% and 14.9% respectively. $WBD has a much greater FCF yield than its competitors. At this valuation I believe the company has been excessively de-risked. With AT&T management out and Discovery's in, I firmly believe David Zaslav & team can successfully unlock shareholder value where the previous management team could not. Building a DCF using projected estimates and margins from the company I come to the conclusion the fair value of the stock is around $70 per share. The stock is currently trading at $17 which indicates its >75% undervalued with a lot of upside potential. This price target is my own and should not be used in your investment decision making. Always do your own research and build your own models.

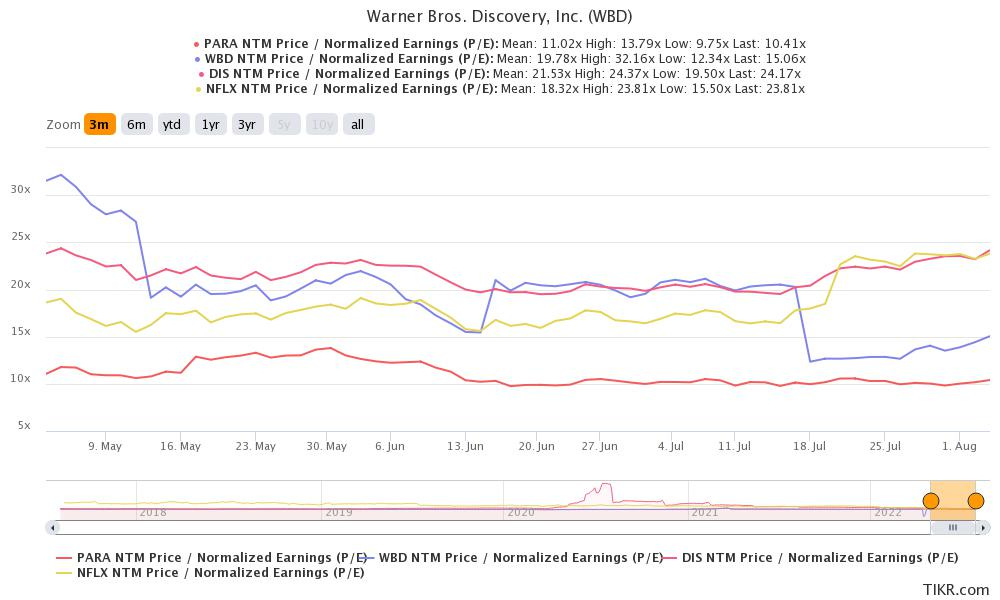

Valuing the company on a P/E basis, WBD 0.00%↑ is one of the cheapest in the group. The library being offered by the combined media company and continued subscriber growth alone should put their P/E more in-line with Disney or Netflix. If I am correct and their P/E is too low, there is plenty of room for multiple expansion.

Brief Technical Analysis:

Price action in WBD 0.00%↑ is unique because the chart shown below corresponds to discovery chart pre merge. The rapid selloff was due to AT&T shareholders selling their WBD 0.00%↑ shares as soon as they received them post merge as well as major share dilution for the combined company. If the daily candle closes above $16.50 then a gap up towards ~$19 could be in store where I would like to see us break out of the down channel outlined below.

Conclusion:

Overall, there are undeniable risks of the current streaming war with giants like AMZN 0.00%↑, NFLX 0.00%↑, DIS 0.00%↑, AAPL 0.00%↑ and many more. Even though the risks are justified, it is extremely hard to ignore the deep value prospects of WBD 0.00%↑. From a valuation standpoint, WBD trades extremely cheap relative to industry averages and deserves a growth rate more in-line with Disney and Netflix. This is because it’s a new media giant that has the resources and scale to compete with its industry peers. It is continuously growing its subscription services while their competitors are starting to decelerate.